Weld partnered with Alty to bring specialised mobile product expertise into the team and launch Ukraine's first crypto-linked payment card in a regulated, high-risk market.

App rating — up from 3.4★

4.7

Active users on GTWorld by 2025

~3M

Growth in new users

+35%

About the Client

Weld is a Ukrainian fintech company focused on enabling practical use of crypto assets for everyday payments

The product allows users to open a card linked directly to their crypto wallet and transact in real time through widely adopted mobile wallets.

The Challenge

Starting conditions increased

execution risk

Weld faced two parallel requirements:

enable real-time crypto spending through mainstream payment channels

ensure onboarding and transactions met regulatory and security expectations

Without experienced leadership in mobile payments and security decisions, Weld risked delays, rework, and an unreliable first release.

Limited in-house mobile product expertise in crypto payments increased reliance on external guidance

Speed and correctness were both critical to launch safely

Enabling real-time transactions through Apple Pay and Google Pay

Reducing onboarding friction

Entering a new, high-risk financial category meant mistakes in security or compliance would be costly

Trial-and-error delivery would introduce unacceptable launch risk

Integrating crypto wallets with traditional payment systems

Meeting regulatory and security standards

Objective

Alty joined Weld as an embedded mobile payments expert, closing the internal capability gap and leading critical product and security decisions. Enable secure crypto payments through mainstream mobile wallets while keeping onboarding simple and compliant.

The strategy prioritised decisions that reduced adoption and compliance risk from day one

Government app Diia integration was chosen to automate identity verification and shorten activation time, reducing onboarding friction and speeding first use.

Apple Pay and Google Pay were prioritised to leverage familiar consumer payment behavior, reducing adoption risk and avoiding the need to educate users on new flows.

Security and compliance were addressed upfront to prevent costly rework and reduce launch risk in a regulated environment.

These decisions removed key uncertainties and enabled a faster, safer launch.

Key design decisions included

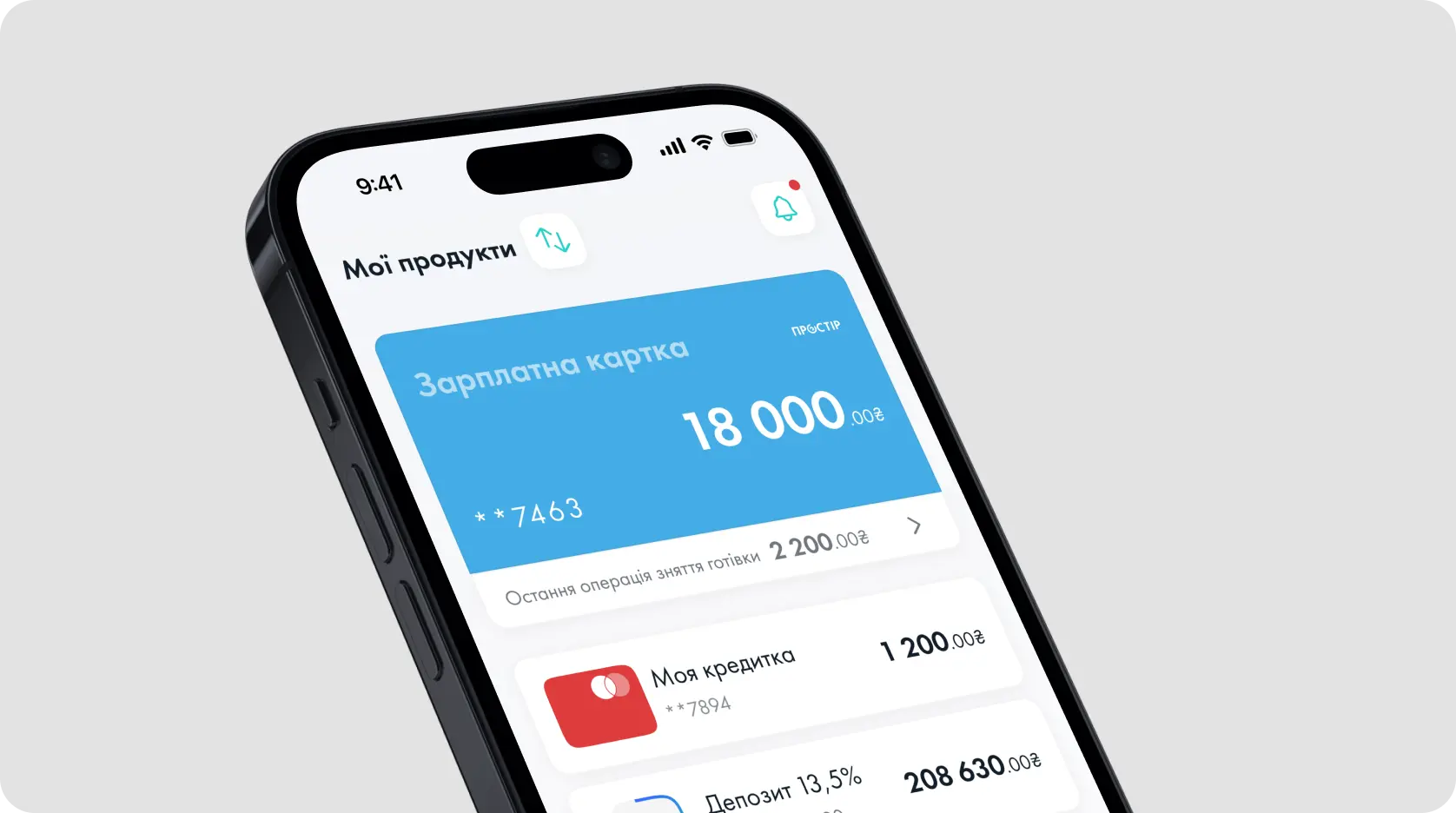

A simplified home structure organised around everyday actions such as products, payments, and transaction history

Personalisation features allowing users to hide rarely used accounts and surface primary products

A redesigned pre-login zone enabling customers to explore services and order cards remotely through national digital identity (Diya) verification

Crypto adoption depends on integration with familiar payment rails, not standalone wallets

Security and compliance are prerequisites for trust in financial products

Reducing onboarding friction accelerates activation more than adding features

Embedded expertise reduces launch risk when entering new, high-stakes categories