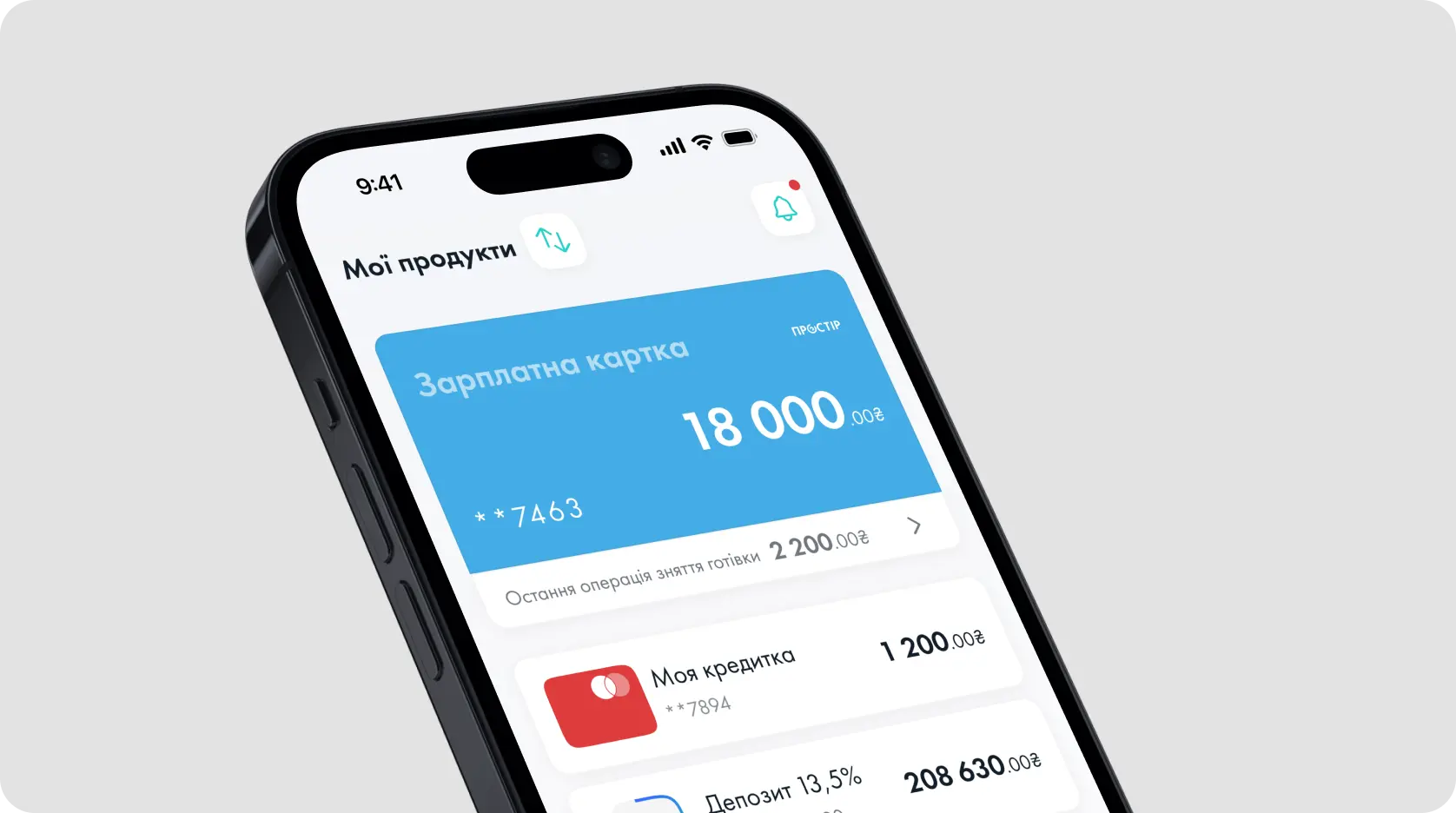

Oschadbank partnered with Alty to reposition its mobile application from a limited digital extension into a primary service channel. The new platform supported the bank’s transition from branch-led operations to digital usage.

App rating — up from 3.4★

4.2

Active users

>4M

About the Client

Oschadbank is one of Ukraine’s largest banks, serving millions of customers across retail banking

For decades, the bank operated primarily through branch-based services and served a broad audience, including many customers less familiar with digital banking.

By 2019, rising demand for remote banking exposed the limits of the existing mobile channel. To reduce operational pressure on branches and maintain relevance across generations, the bank required a scalable digital alternative that preserved familiar banking logic.

The Challenge

Structured migration strategy from branch-based service to digital channels

Oschadbank’s first mobile application had been launched more than ten years earlier and supported only basic banking tasks. Most customers continued to rely on branches for everyday operations, and mobile usage remained limited to a narrow set of functions.

The core challenge was not technology alone. Oschadbank needed to shift millions of customers from branch-based service to digital channels while preserving familiarity, trust, and accessibility for users with low digital confidence.

This created a complex operating-model problem. Without a structured migration strategy, mobile banking would remain a secondary utility, leaving branch traffic and servicing costs structurally high.

Branch traffic remained high, sustaining operational cost and manual servicing

Designing a mobile product usable by both digitally fluent and low-confidence users

Younger and digitally fluent users expected a modern, self-service mobile experience

Reducing dependence on physical branches while preserving familiar banking logic

Existing customers risked being excluded if the digital transition moved too fast

Repositioning mobile banking from a basic utility to a primary service channel

Migrating a predominantly branch-first customer base to digital channels without disrupting trust

Objective

Alty joined Oschadbank as a product strategy and experience partner, focusing on defining the role of mobile banking in the bank’s future operating model.

Alty conducted a detailed review of the existing mobile product together with Oschadbank’s teams and customers. Interviews and usability analysis revealed that customers continued relying on branches or moved funds to other banks because key everyday functions were missing or difficult to use.

The analysis identified structural drivers

Branch dependency was driven by missing digital capabilities, not customer resistance

Users of all ages were willing to adopt mobile banking if core tasks were simple and reliable

Mobile had to replicate everyday branch workflows before introducing advanced services

The engagement focused on structural decisions

The new app would operate as a full alternative access channel rather than a limited extension of branch systems.

Design for gradual migration, not abrupt replacement.

The experience had to preserve familiar banking logic while introducing modern interaction patterns, enabling customers to shift behaviour progressively.

Position mobile as the primary entry point for everyday banking.

The app would focus on payments, transfers, savings, and daily transactions to reduce reliance on branches over time.

Based on these findings, the mobile app was positioned as a practical service channel for routine banking rather than a niche digital product for early adopters.

Collaboration & Ownership

Alty led discovery and structured the modernization roadmap, aligning stakeholders and removing decision fragmentation across teams.

The Results

Reduced branch dependency for routine payments and transfers

Lowering operational servicing pressure

Infrastructure modernization reduced long-term maintenance costs while improving platform stability and scalability

App rating — up from 3.2★,

reflecting improved usability and trust

4.2

Active mobile users, establishing digital as a primary channel

4M+

In transactions in 2022

₴250B

Daily visits

~500,000

“

It’s been four years of our fruitful cooperation with Alty. We love the team and happily refer Alty to our network.

Volodymyr Moskalenko,

Director of E-commerce and Payments

Remote channel adoption grows when everyday banking is structured around familiar actions rather than advanced features

Designing for customers with low digital confidence expands digital reach beyond early adopters

UX-led product direction can support digital growth even when technical delivery remains internal

Personalisation controls help serve broad audiences without fragmenting the interface