Monobank launched in 2017 with an ambition to build a fully digital bank in a market shaped by post-crisis distrust and branch-centric banking. Alty helped define the experience architecture behind a mobile-first banking model that later scaled to more than 8 million users.

App rating. Sustained user satisfaction at scale, Confirmed that clarity-driven design translated into long-term behavioral trust

4.9

Active users. Demonstrated that mobile-only banking could achieve mass adoption without branch infrastructure.

>8M

Competitive displacement of traditional branch-centric banks. Proved structural viability of a digital-first retail banking model.

Market Leadership Position

About the Client

Monobank is Ukraine’s leading neobank, launched in 2017 to disrupt a market dominated by traditional, branch-centric banks

At the time of launch, customer trust in banks was low, service expectations were shaped by bureaucracy and inefficiency, and mobile apps often replicated legacy processes rather than improving them.

Market conditions were increasingly favourable for a mobile-first alternative: users were fatigued by poor service, ready to adopt digital-first models, and open to banks that could combine transparency, speed, and reliability. Monobank entered the market at this inflection point, with a clear ambition to redefine everyday banking.

The Challenge

The challenge was not adding features.

It was defining a digital banking model customers could understand, trust, and use daily

Failure would not only slow adoption – it would invalidate the digital-only operating model. Without early trust formation, customer acquisition costs would rise, regulatory scrutiny would intensify, and the absence of branch infrastructure would become a structural liability rather than an advantage.

Monobank did not face a typical “app design” problem. It faced a structural market question:

Could a bank operate entirely through a mobile interface in a trust-constrained environment?

At the time:

Traditional banks relied heavily on branches

Mobile apps were secondary and often poorly structured

Customers associated banking with paperwork, queues, and opaque processes

Launching as a digital-only bank introduced significant risk:

No physical reassurance layer

No legacy trust cushion

No fallback to branch-based service

If the mobile experience failed to establish clarity and confidence immediately, adoption would stall.

What interaction model builds trust without physical presence?

How can digital onboarding feel immediate but secure?

How should a mobile-only bank structure everyday banking without branch logic?

How should financial products be presented to reduce friction rather than increase cognitive load?

Objective

Alty joined Monobank at a critical model-definition stage, leading the experience architecture and defining the interaction logic required to operationalize a mobile-only banking system under trust-sensitive conditions.

The work focused on structural decisions rather than visual redesign.

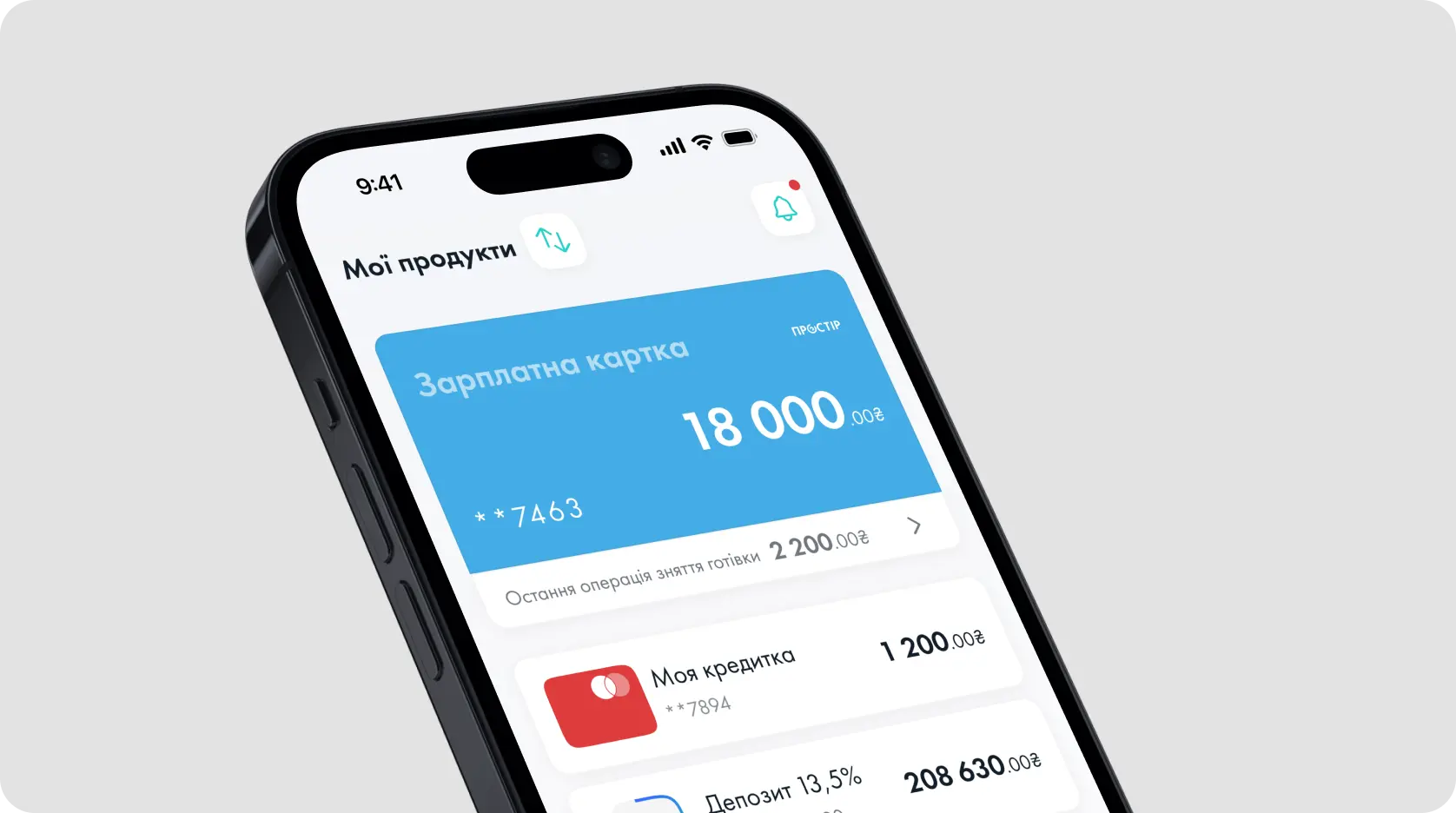

1. Mobile as the Primary Operating Model

Rather than replicating traditional banking interfaces, the product was structured around everyday financial behavior:

Card-first logic

Clear transaction visibility

Immediate feedback loops

Transparent limits and balances

Insight

Users associated banking complexity with institutional opacity and risk.

Decision

Core interactions were reorganized around a card-first, real-time transaction model.

Business effect

Reduced cognitive friction and accelerated habit formation, reinforcing mobile as the primary banking surface.

This eliminated branch-derived navigation logic embedded in traditional banking apps.

2. Simplicity as a Trust Mechanism

In a market shaped by institutional distrust, clarity became a strategic instrument. Instead of layering advanced features at launch, the product emphasized:

Predictable flows

Minimal cognitive overload

Immediate confirmation of actions

Visible control over finances

Insight

In a post-crisis environment, perceived clarity directly influenced perceived safety.

Decision

Feature expansion was intentionally constrained at launch in favor of predictable flows and visible financial control.

Business effect

Trust formation became embedded in interaction design rather than dependent on physical reassurance.

Simplicity was not aesthetic. It was structural risk mitigation.

3. Digital Onboarding Without Friction

Account opening and activation were engineered to minimize delay while preserving regulatory compliance.

The objective was behavioral: shorten the gap between curiosity and first meaningful use.

Insight

The longer the gap between intent and activation, the higher the abandonment risk in a digital-only model.

Decision

Decision

Onboarding was streamlined to compress time-to-first-use without compromising compliance integrity.

Business effect

Reduced acquisition leakage at the most fragile stage of the customer journey.

The Results

Large-scale validation of a fully digital banking model in a trust-constrained market

Sustained user satisfaction at scale. Confirmed that clarity-driven design translated into long-term behavioral trust

4.9

Active users. Demonstrated that mobile-only banking could achieve mass adoption without branch infrastructure.

>8M

Competitive displacement of traditional branch-centric banks. Proved structural viability of a digital-first retail banking model.

Market Leadership Position

“

We have been collaborating with the Alty team since 2010 and firmly believe they are the best in the market. Their unmatched expertise was the primary reason we chose them to design Monobank back in 2017.

Misha Rogalskiy, Co-founder at The Credit Thing and Monobank

Key Takeaways

01

Digital trust is earned through simplicity, not feature volume

02

User-centric design can reset expectations in even the most traditional markets

03

Viral growth emerges when everyday banking feels effortless and human

04

Neobanks scale faster when mobile is the primary, not secondary, channel